If you want to make more than 5% interest these days, you are going to need to look at something other than stocks and bonds.

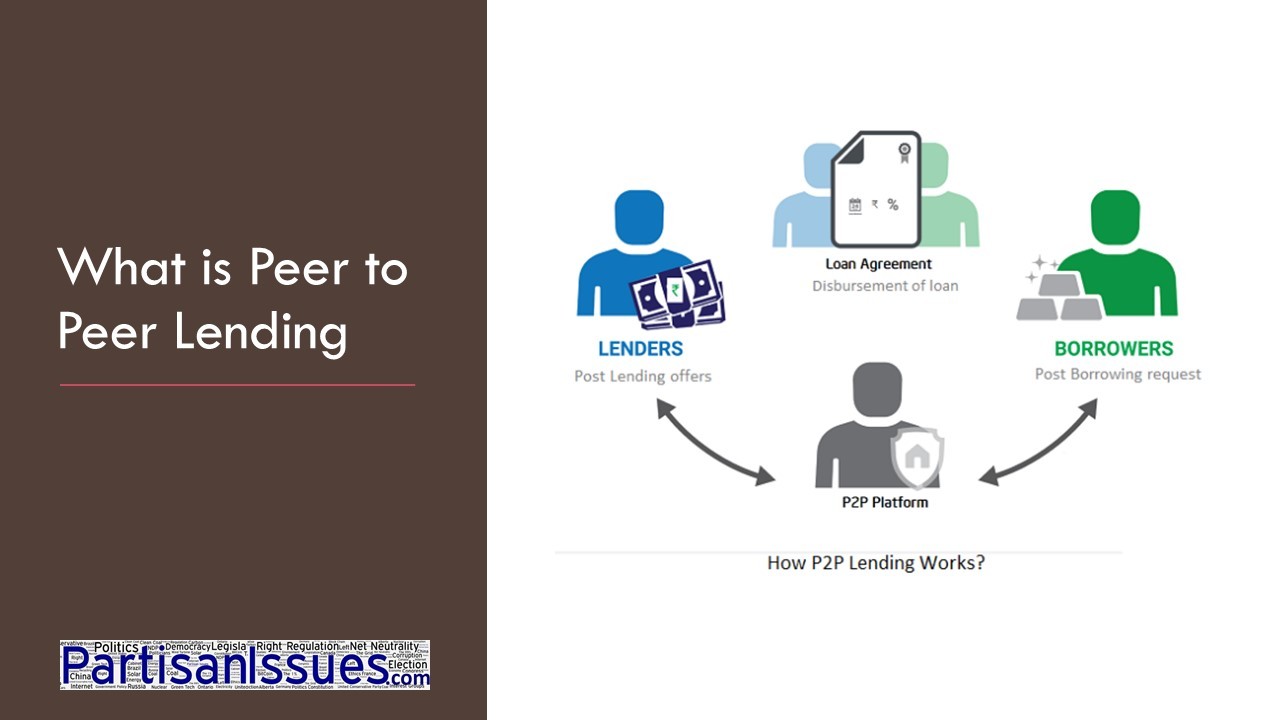

In the simplest terms, Peer to Peer Lending connects borrowers with lenders directly. The idea is to remove large and slow banks that typically collect deposits and lend money, from the equation and allow lenders and borrowers to talk directly.

Banks have so many rules and regulations to follow (which is a good thing because they are typically stable… lets just ignore 2007/8) they add substantial cost and reduce efficiency.In todays fast moving business world and low interest rate environment, the time is right for P2P transactions.

P2P services are part of the broader Financial Technology (aka ‘FinTech’) industry you have heard so much about in recent years.

In this video we explain the positives and negatives of Peer to Peer Lending as well as provide real world examples:

Am I Buying Shares in the Peer To Peer Lending Firm?

People interested in Peer To Peer Lending firms are often initially confused about what they are investing in. You are not an investor in the P2P company (like Upstart, Funding Circle, Prosper, LendingLoop.ca, Kuflink, RateSetter, i2iFunding, …). Those companies are just managers and a transit point for your money. You are loaning money to companies that are requesting loans through the P2P firm. The P2P Lending company does not put their money into the loans; they just:

- handle the applications

- verify information (hopefully!)

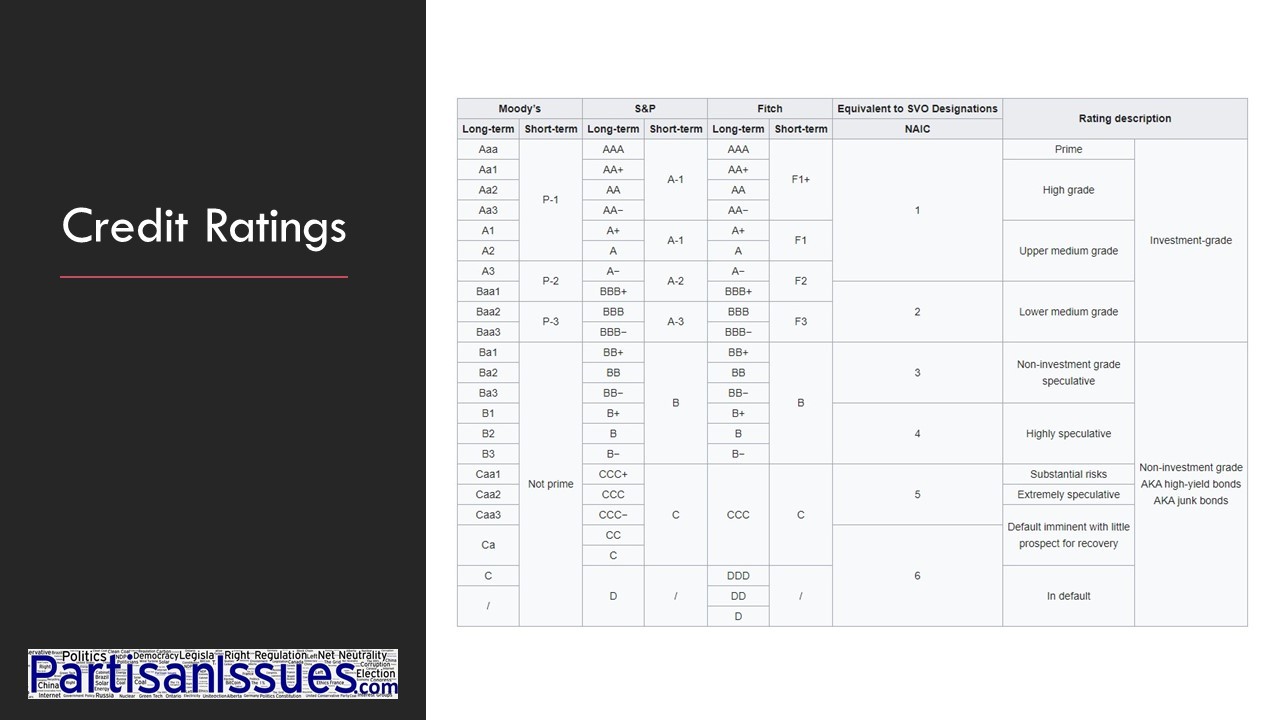

- assign a credit worthiness score and matching interest rate

- provide the money from multiple lenders (to reduce individual risk)

Click to Expand Graphic

PEER TO PEER LENDING POSITIVES:

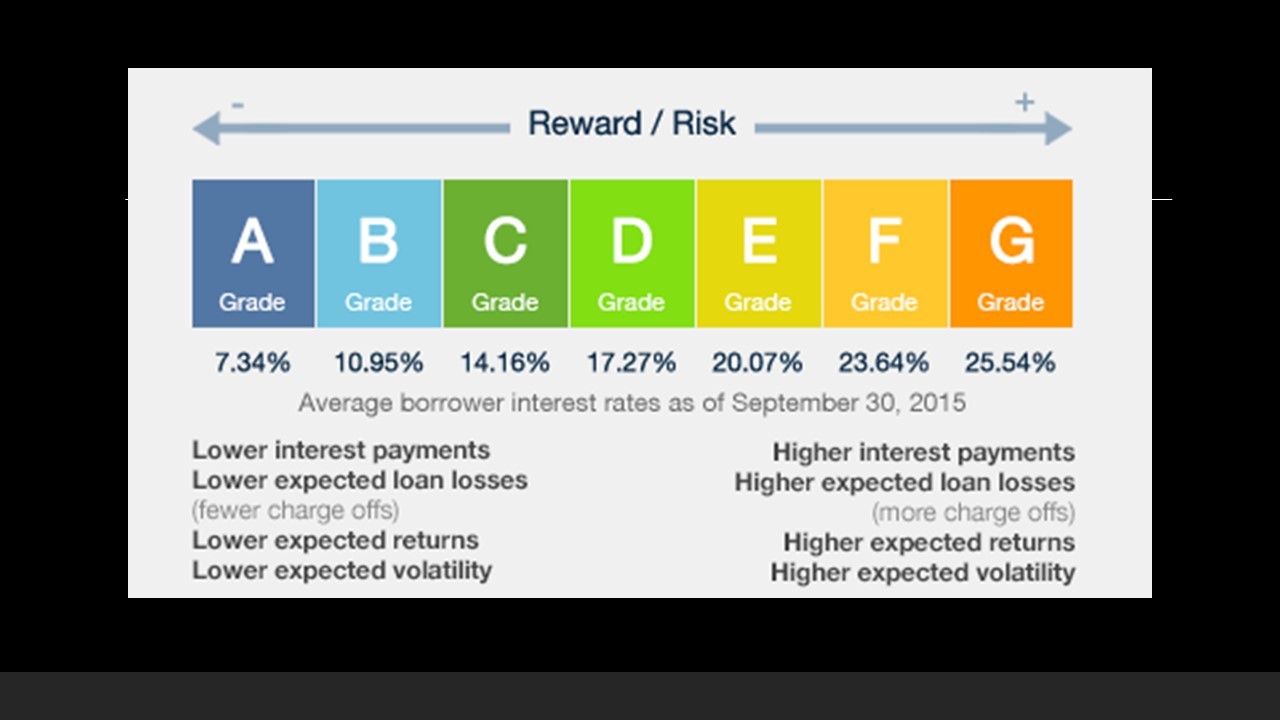

- Interest Rates aka Returns are by far the most important reason to get into P2P lending

- Borrowers seldom pay below 10% and often pay closer to 20%

- Some P2P companies lend to people but most are corporate only and that is a good thing

- still risky

- but even small companies have some vetting from trade creditors, family and friend lenders

- have more reason to pay back

- Not directly correlated to stock market but if the stock market drops, that likely means the economy is dropping and that means your lendee is more likely to have business decline which means they are less likely to payback

- Less messy that Bond ETF’s because ETF’s trade bonds mid cycle and these are held to maturity

- New asset class to diversify

- Supporting small business or your local economy

PEER TO PEER LENDING NEGATIVES:

- Lending to companies that can’t get loans from banks

- Risk – about 10% go bad and sell off at about $10 on the dollar – less fees so, zero

- In most countries, P2P profits are taxed as regular income not as dividend income (which is often taxed at half rate)

- P2P Lenders often state they are not required to verify applicant’s information

- one of the US companies says they are not required to verify income and may lend based on stated income think housing bubble

- likely just covering their butt legally but still not a good sign

- one of the US companies says they are not required to verify income and may lend based on stated income think housing bubble

- You are typically an unsecured investor

- Limited or no secondary markets so your P2P investments are not liquid

2 Comments

Anna rose jiang · November 10, 2020 at 11:05 am

hello

How to application Loans international financial worldwide what it’s inquiry for application Loans international financial worldwide

I’m looking forward thank you for your kindly reply ASAP

Best regards

Anna rose jiang

Ian Matthews · November 12, 2020 at 11:38 am

Hi Anna Rose; I suggestion you contact your in-country peer to peer lending service. I don’t think most peer to peer lenders provide funds outside of their territory because they need to have local knowledge to make informed lending decisions. There may be a few exceptions like https://www.lendingworks.co.uk/ .

I hope that helps.